7: The Sausage Empire, Catching the Madoff Knife Mid-Air, LG Deserves Better, Coinbase Unhappening, How Rome’s Collapse Fueled Modernity

7: The Sausage Empire, Catching the Madoff Knife Mid-Air, LG Deserves Better, Coinbase Unhappening, How Rome’s Collapse Fueled Modernity

Everything we see hides another thing, we always want to see what is hidden by what we see - René Magritte

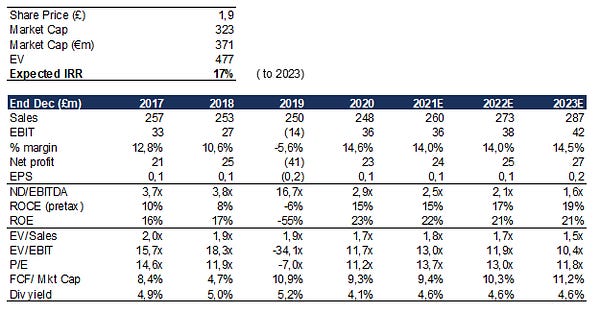

This week, I published a deep-dive on Devro, a UK listed sausage casings manufacturer, on my research blog dedicated to searching for the root cause:

Elevator pitch:

I would like to present you Devro Plc, a UK-listed small cap company operating in an oligopolistic market under a disciplined leader (Viscofan $VIS). Thanks to great underlying trends in the collagen casings market (and more broadly in per capita meat consumption), especially in Emerging Markets, Devro offers a compelling investment opportunity where you basically get paid a 5% cash dividend for waiting for a re-rating to materialize, which I estimate could happen between the end of 2023. That scenario will net you a c.15% IRR through the end of 2023 in my base case where the stock re-rates from 10.4x EV/EBIT to 12.4x EV/EBIT, and up to 40% until through the end of 2023 in my "dream" case, where the stock re-rates to 15.4x EV/EBIT (still significantly lower than Viscofan $VIS).

Disclaimer: Long $DVO.

Investing & Business

Catching the Madoff Knife Mid-Air in 2001

Reading time: ~10 minutes

With the announcement of Madoff’s death in prison this week, the whole story was brought into the spotlight again, with some interesting content resurfacing.

One of them is this article featured in Barron’s in 2001, written by Erin E. Arvedlund:

Back then, a few years before one of the biggest collapses in recent financial history, investors were naming Madoff as the go-to investment manager in the space. At that time, Madoff Securities was even the third-largest market-making firm (matching sell and buy orders on NYSE-listed securities for a fee).

His clout allowed Madoff to get away with some… pretty vague explanations to say the least:

What few on the Street know is that Bernie Madoff also manages $6billion-to-$7 billion for wealthy individuals. That's enough to rank Madoff's operation among the world's three largest hedge funds, according to a May 2001 report in MAR Hedge, a trade publication.

What's more, these private accounts, have produced compound average annual returns of 15% for more than a decade. Remarkably, some of the larger, billion-dollar Madoff-run funds have never had a down year.

When Barron's asked Madoff Friday how he accomplishes this, he said,"It's a proprietary strategy. I can't go into it in great detail."

When probed further about the exact nature of his fund’s strategy by investors, journalists, and experts in the space, Madoff proceeded to sketch out a strategy revolving around buying some of the S&P500 biggest securities combined with call & put options on the underlying to handle volatility and stabilize returns, a strategy called “split-strike conversion”.

However, many professionals with knowledge of the strategy were simply not taking it:

Some on Wall Street remain skeptical about how Madoff achieves such stunning double-digit returns using options alone. The recent MAR Hedge report, for example, cited more than a dozen hedge fund professionals, including current and former Madoff traders, who questioned why no one had been able to duplicate Madoff's returns using this strategy. Likewise, three option strategists at major investment banks told Barron's they couldn't understand how Madoff churns out such numbers.

The essay concludes with a warning that has aged well over the following years, about the lessons that one should have learned from the previous high-profile meltdown of Long Term Capital Management:

The lessons of Long-Term Capital Management's collapse are that investors need, or should want, transparency in their money manager's investment strategy. But Madoff's investors rave about his performance --even though they don't understand how he does it. "Even knowledgeable people can't really tell you what he's doing," one very satisfied investor told Barron's. […] This investor declined to bequoted by name. Why? Because Madoff politely requests that his investors not reveal that he runs their money.

"What Madoff told us was, 'If you invest with me, you must never tell anyone that you're invested with me. It's no one's business what goes on here.

LG Deserves Better (and so do you)

Reading time: ~30 minutes

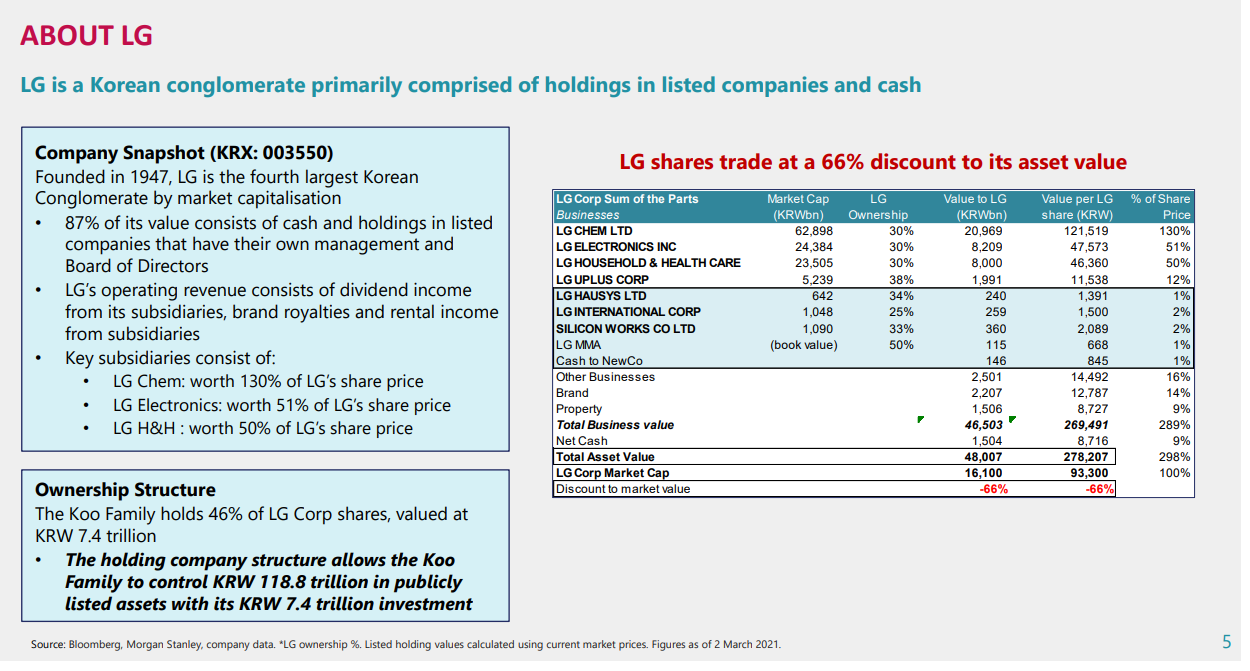

In Korea, the stock market is dominated by family-owned conglomerates, called "chaebols”:

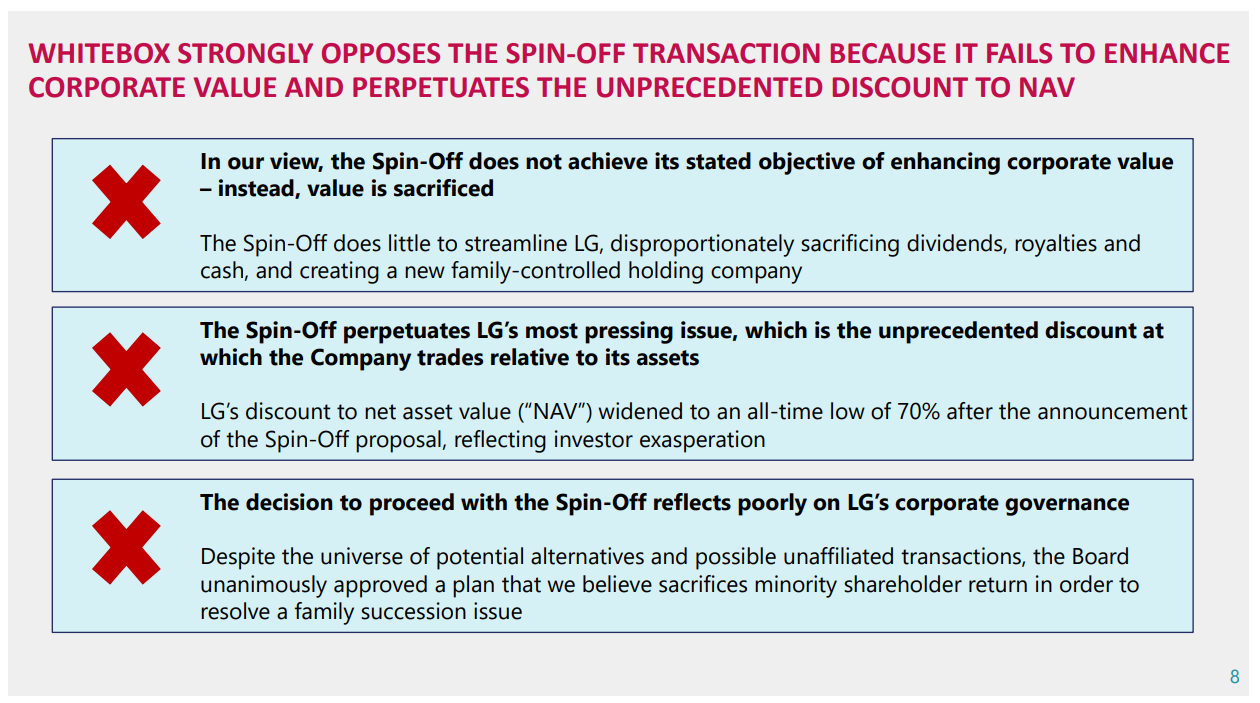

Whitebox Advisors, an activist fund, published a presentation to try to oppose the planned LG spin-off, which is more motivated by the the desire to help a member of the founding family to start his own business rather than enhance shareholder value:

The presentation gets quite a few points across, especially about the technicals of the proposed spin-off:

Minimal transfer in terms of percentage of total assets (~2%)

Disproportionate effect in terms of revenues (~10% of revenues spun-off) and cash reserves (~9% of cash holdings spun-off) which hurts minority shareholders of the conglomerate

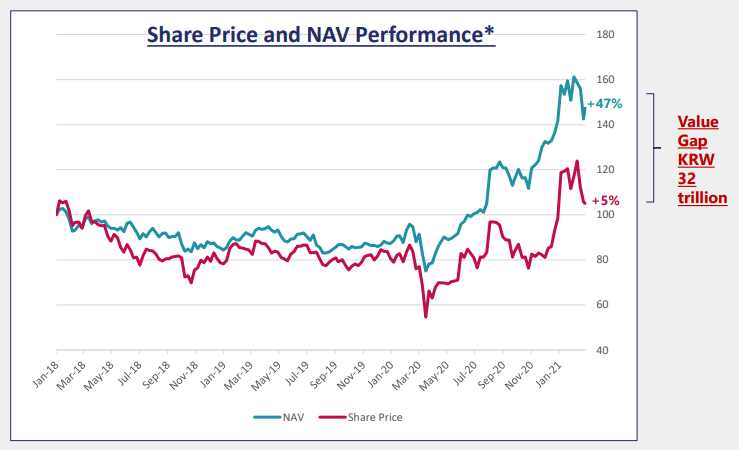

While Korean conglomerates are generally hostile to minority shareholders, LG trades at an unprecedented discount to NAV even when compared with peers, which has been very detrimental to shareholders over the last few years:

Whitebox proposals include:

1) the abandon of the spin-off

2) the implementation of better governance principles

3) the implementation of a real capital allocation plan.

Thought-provoking stuff…

Coinbase “Unhappening”

Reading time: ~10 minutes

Scott Galloway, emeritus professor at NYU teaching marketing, was recently interviewed by the New York Magazine to (sort of) give his unified view of what’s happening currently, in the markets and more broadly.

Insight #1: The Techno-fiscal moment

It’s likely that the Wall Street firms, realizing they ceded too much of a head start to compete on the whole “innovation” thing, will weaponize their lobbyists to convince regulators to shift their gaze away from SPACs (harmless fun) and focus on the existential threat(s) of crypto.

Prediction: congressional hearings on crypto where committee members make the previous hearings on big tech look elegant and informed.

On what happens next in the space after the landmark $COIN IPO, Galloway is not really sanguine, and I would say it makes sense when you take a step back and seize fully the level of internal contradiction of what is happening under our gaze:

In an AOL-like move (another early on-ramp to the future), Coinbase might unhappen. One of the tenets of crypto is decentralization, which doesn’t bode well for a middleman that charges 1990s-esque fees. (Coinbase fees can be over 4% per transaction, 10x or more the fees charged by competitors.)

In an AOL-like move (another early on-ramp to the future), Coinbase might unhappen. One of the tenets of crypto is decentralization, which doesn’t bode well for a middleman that charges 1990s-esque fees. (Coinbase fees can be over 4% per transaction, 10x or more the fees charged by competitors.)

Insight #2: Negative Externalities

The increased baseline level of volatility across asset classes is the rallying cry of an unease that sits deeper:

People under the age of 40 are fed up. […] For the first time in our nation’s history, a 30-year-old isn’t doing as well as his or her parents were at 30. That creates shame and rage in households across America.

The credible-scarcity component of our existing currencies — they’re losing the credibility part. When the government decides to print $4 trillion in debt, in new money that we don’t really have a discernible plan to pay back, the USD is losing its scarcity cred.

The problem, both Galloway and his interviewer agree on, is that the kind of disruptive innovation we’ve been witnessing is only likely to further increase the level of wealth inequality. To put it in simple words, You cannot YOLO your savings if you don’t have savings to start with, right?

All of this heads toward a dystopian future where income inequality is going to get even greater. And we’re going to have to get used to the notion of redistribution of income or make a massive investment in retraining or vocational education for young people.

I think the last part is really interesting on its own, and reminds me a lot of the NYT essay “Reopening an Employment Door to the Young”, published in 2014. Specifically, this part:

Twenty or thirty years ago, a hiring manager at a F500 company was much more willing to give, say, a dance major a chance. That manager would realize that such graduates were good at teamwork, acquiring new skills and practicing for long hours. Give them some corporate training and they become productive employees, was the thinking.

Now, because of a relentless focus on specialized skills, too many young people are missing out on a rite of passage: getting to a job on time, learning a craft, assuming responsibility, bringing home a paycheck. The unemployment rate for people age 20 to 24 is 11 percent, compared with an overall rate that is under 7 percent.

It’s not that they aren’t trying to find work. One problem is that young people are competing both with their peers and with experienced applicants willing to accept entry-level salaries.

Arts & History

How Rome’s Collapse Fueled Modernity

Reading time: ~20 minutes

In this essay, the authors explore the unexpected role the fall of the Roman empire had in planting the seeds of modernity in Europe. Really well written and informative piece. Here are my selected highlights:

All these enduring influences pale against Rome’s most important legacy: its fall. Had its empire not unravelled, or had it been replaced by a similarly overpowering successor, the world wouldn’t have become modern.

In French Theory’s #4 Edition, I wrote about the heritage that History as a science owes to both Herodotus and Thucydides, and how their ideological relationship modeled the science around revisionism. Here, I picked up an interesting comment resonating very well with this previous insight:

Back in 1984, the German historian Alexander Demandt patiently compiled no fewer than 210 different reasons for Rome’s demise that had been put forward over time. And the flood of books and papers shows no sign of abating: most recently, disease and climate change have been pressed into service. Wouldn’t only a calamity of the first order warrant this kind of attention?

As a bonus, the last sentence also resonates with the debate between histoire totale and histoire événementielle! The essential idea conveyed by the essay is that similarly to how burned soil can prove more fertile, the fall of the Roman Empire created the perfect chaos to ensure modernity would sprout:

For much of the Middle Ages, power was widely dispersed among different groups. […] The resultant landscape was a patchwork quilt of breathtaking complexity. […] So many different power structures intersected and overlapped, and fragmentation was so pervasive that no one side could ever claim the upper hand; locked into unceasing competition, all these groups had to bargain and compromise to get anything done. Power became constitutionalised, openly negotiable and formally partible; bargaining took place out in the open and followed established rules.

Finally, I wanted to highlight the last paragraph, which wraps the whole essay wonderfully:

Long before our species existed, we caught a lucky break. If an asteroid hadn’t knocked out the dinosaurs 66 million years ago, our tiny rodent-like ancestors would have had a hard time evolving into Homo sapiens. But even once we had gotten that far, our big brains weren’t quite enough to break out of our ancestral way of life: growing, herding and hunting food amid endemic poverty, illiteracy, incurable disease and premature death. It took a second lucky break to escape from all that, a booster shot that arrived a little more than 1,500 years ago: the fall of ancient Rome.

Treat for the Ears

My GF just came into my office to tell me something, and I had to let her know it would need to wait because I was dealing with a FUNK EMERGENCY

Other Interesting Links

Manger, boire, rigoler, découvrir. La vie aussi #cestmeilleurquandcestbon

Incredible Youtube channel about (mostly) French cuisine I discovered this week!

Until next week,

Antoine